Global Economics News Update

Further Reading

Global Economics Update provided by Australian market analyst UBS.

Global Economics – Turning the corner

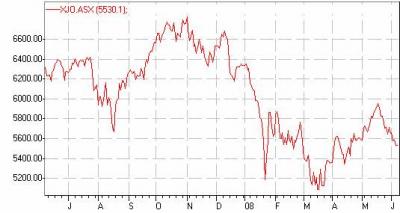

There is no doubt the Aussie market has seen some tough times in the last year, as the chart below shows. The US credit crunch and the associated confidence crisis that it brought about has had a serious detrimental effect not just on their own market, but on markets across the globe. Fears of a recession in the worlds largest consumer economy has driven fears of a deep global recession.

However, we have seen some positive economic signals emerging from the US economy of late that suggest the worst may be over. Is it time to dip the toe back in the investment waters again? In this note we examine recent global economic releases and examine whether they can provide us with any future direction for global and domestic markets.

Source: IRESS Daily

US Figures

US GDP growth was revised up in the last week to a preliminary annualised estimate of 0.9% from an advanced reading of 0.6%. Housing growth remained a major drag on the economy, however, exports provided a positive counterbalance, adding 0.8 percentage points to growth. Inventories also made a positive 0.2 percentage point contribution. The key point here is that a dreaded recession requires consecutive quarters of negative GDP growth. The Q1 positive GDP growth must be viewed as a move in the right direction.

Production also put in a strong quarter, with the ISM index up 1pt in the quarter suggesting the low point in manufacturing may have been reached. Factory Orders rose 1.1% in April, and non-manufacturing ISM business activity index also rose 1.6pts in April. Both these results further highlight the trend and support an argument that the worst may be over.

EURO Figures

1Q EURO area GDP growth was revised up to a preliminary reading of 0.8% from initial estimates of 0.7%. Euro area Economic sentiment was unchanged with weaker consumer sentiment offset by confidence improvements in Services Construction and Retail. Euro unemployment remained steady at 7.1%.

Inflation remains a nightmare in the Euro Area running at ~3.6% vs ECB’s inflation target of 2%

U.K.

U.K. Manufacturing PMI fell to 50.0 from 50.8 in April, however the headline rate is not at a particularly low level by historical standards.

U.K consumer confidence numbers deteriorated with falling house prices, rising mortgage rates and soaring energy and food costs all likely to be weighing on sentiment.

Japan

Weaker corporate revenues, capital spending and softer sentiment point to slowing activity, although any downturn does not look severe.

So…. where to from here?

Inflation remains the key concern, particularly in Europe. There are also inflation concerns immerging in the US, with the Fed hinting that they are done with rate cuts as inflation concerns build. Fed payroll data will be watched with interest tonight. A bad number with little prospect of a rate cut could see a nasty sell-off. A good number would further support the string of recent data suggesting the worst may be over.

Watch this space…..

- How to Trade Forex and Gold Options

- How to Trade the Gold Price and Profit!

- Forex Trading the EUR/USD Pair € EURO and $ US Dollar

- How to Trade Stock Market Indices S&P500

- How to Trade Crude Oil

- Forex Trading Psychology

- What Are Broker Recommendations?

- Free Tickets to Trading & Investing Seminar & Expo ($18) Brisbane 2013

- Stock Calc App

- All About Warrants

- Introduction to Exchange Traded Funds

- Introduction to Exchange Traded Funds: Features

- Introduction to Exchange Traded Funds: Domestic ETFs

- Introduction to Exchange Traded Funds: International ETFs

- Exchange Traded Commodities

- Australian Stock Scan

- Australian Online Share Trading

- List of Trading Books

- Interesting Thoughts about the Australian Dollar

- What's the Meaning of Hawkish?

- Do You Know How To Use the P/E Ratio

- Trading, Religion and Politics - Do They Have Anything in Common?

- Shares that are Volatile that Double and Half in the Short Term

- Telstra (TLS) T3

- Margin Call by E-mail

- The Cost of Holding a Position

- Lack of Disclosure: Compensation from ASX Listed Company

- Unrealistic Returns and Benchmarks

- CMC Markets Down

- Quality versus Quantity Forex Trading

- Woolworths 1H Sales $30.7bn up 3.2%

Date added 31-01-2013 - ASIC Fines CommBank's CommSec

Date added 25-09-2012 - Industry Super Network Calls to Ban High Frequency Trading (HFT)

Date added 22-09-2012 - NAB Launches Online Share Trading Platform

Date added 19-09-2012 - Reserve Bank of Australia Says 23 Countries Holding AUD

Date added 18-09-2012 - Australia Post Digital Mailbox

Date added 10-09-2012 - Winners and Losers of Trading for Week 2

Date added 16-01-2012 - 2012's First Week of the Best and Worst Traded Stocks

Date added 09-01-2012 - 2011's Last Best and Worst Traded Stocks

Date added 05-01-2012 - Best and Worst Pre-Christmas Traded Stocks

Date added 30-12-2011 - Trading Winners and Losers for Dec. 12-16

Date added 19-12-2011 - Best and Worst Traded Stocks for Dec. 5-9

Date added 13-12-2011 - Top 3 Best and Worst Traded Stocks

Date added 05-12-2011 - ASX Glitch Trading Halt

Date added 27-10-2011 - Worst Trade Stocks (and the Best)

Date added 06-08-2011

Top 150 Public Companies Listed on the Australian Stockmarket as at 29/05/2009

- BHP Billiton

- Westpac Banking Corporation (WBC)

- Commonwealth Bank of Australia (CBA)

- National Australia Bank (NAB)

- Telstra (TLS)

- ANZ

- News Corporation (NWS)

- Woolworths Limited(WOW)

- Woodside Petroleum Limited (WPL)

- Rio Tinto

- Westfield Group (WDC)

- Westfarmers Limited (WES)

- QBE Insurance

- CSL

- Newcrest Mining Limited (NCM)

- Origin Energy Limited (ORG)

- Santos Limited (STO)

- AMP Limited (AMP)

- Macquarie Group (MQG)

- Foster’s Group Limited (FGL)

{kind=link}